To make a product profitable, the remaining income after variable costs must be more than the company’s fixed costs, such as insurance and salaries. Thus, the level of production along with the contribution margin are essential factors in developing your business. Now, it is essential to divide the cost of manufacturing your products between fixed and variable costs. The contribution margin is the foundation for break-even analysis used in the overall cost and sales price planning for products. Here, the variable costs per unit refer to all those costs incurred by the company while producing the product.

Formula For Contribution Margin

Remember, the per-unit variable cost of producing a single unit of your product in a particular production schedule remains constant. When only one product is being sold, the concept can also be used to estimate the number of units that must be sold so that a business as a whole can break even. For example, if a business has $10,000 of fixed costs and each unit sold generates a contribution margin of $5, the company must sell 2,000 units in order to break even. However, if there are many products with a variety of different contribution margins, this analysis can be quite difficult to perform.

Formula to Calculate Contribution Margin Ratio

It is an important input in calculation of breakeven point, i.e. the sales level (in units and/or dollars) at which a company makes zero profit. Breakeven point (in units) equals total fixed costs divided by contribution margin per unit and breakeven point (in dollars) equals total fixed costs divided by contribution margin ratio. For the month of April, sales from the Blue Jay Model contributed $36,000 toward fixed costs. Looking at contribution margin in total allows managers to evaluate whether a particular product is profitable and how the sales revenue from that product contributes to the overall profitability of the company. In fact, we can create a specialized income statement called a contribution margin income statement to determine how changes in sales volume impact the bottom line.

Is contribution margin the same as profit?

In these examples, the contribution margin per unit was calculated in dollars per unit, but another way to calculate contribution margin is as a ratio (percentage). Using this formula, the contribution margin can be calculated for total revenue or for revenue per unit. For instance, if you sell a product for $100 and the unit variable cost is $40, then using the formula, the unit contribution margin for your product is $60 ($100-$40). This $60 represents your product’s contribution to covering your fixed costs (rent, salaries, utilities) and generating a profit.

If a company uses the latest technology, such as online ordering and delivery, this may help the company attract a new type of customer or create loyalty with longstanding customers. In addition, although fixed costs are riskier because they exist regardless of the sales level, once those fixed costs are met, profits grow. All of these new trends result in changes in the composition of fixed and variable costs for a company and it is this composition that helps determine a company’s profit.

Fixed cost vs. variable cost

- It even plays a vital role in break-even analysis, helping you pinpoint exactly when your venture will start turning a profit.

- You will also learn how to plan for changes in selling price or costs, whether a single product, multiple products, or services are involved.

- This \(\$5\) contribution margin is assumed to first cover fixed costs first and then realized as profit.

- When the contribution margin is calculated on a per unit basis, it is referred to as the contribution margin per unit or unit contribution margin.

Net sales refer to the total revenue your business generates as a result of selling its goods or services. Furthermore, a higher contribution margin ratio means higher profits. This means that you can reduce your selling price to $12 and still cover your fixed and variable costs. Yes, the Contribution Margin Ratio is a useful measure of profitability as it indicates how much each sale contributes to covering fixed costs and producing profits.

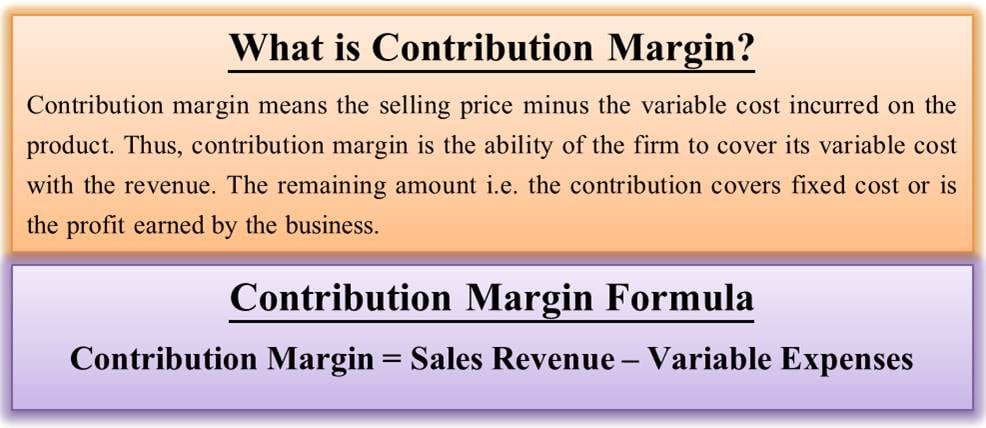

The formula to calculate the contribution margin is equal to revenue minus variable costs. Raw materials, hourly wages and shipping costs are classic examples. A bakery that doubles its cake production will see its flour and sugar expenses rise accordingly. This direct relationship between activity level and cost gives businesses flexibility but also requires careful management to maintain profitability as production scales up or down. In May, 750 of the Blue Jay models were sold as shown on the contribution margin income statement. When comparing the two statements, take note of what changed and what remained the same from April to May.

On the other hand, contribution margin refers to the difference between revenue and variable costs. At the same time, both measures help analyze a company’s financial performance. However, an ideal contribution margin analysis will cover both fixed and variable cost and help the business calculate the breakeven.

This means that $15 is the remaining profit that you can use to cover the fixed cost of manufacturing umbrellas. Also, you can use the contribution per unit formula monitor cash positions and manage liquidity camden national bank to determine the selling price of each umbrella. Contribution Margin refers to the amount of money remaining to cover the fixed cost of your business.